Call us on 020 7183 2277

Download LATEST Market Rates >

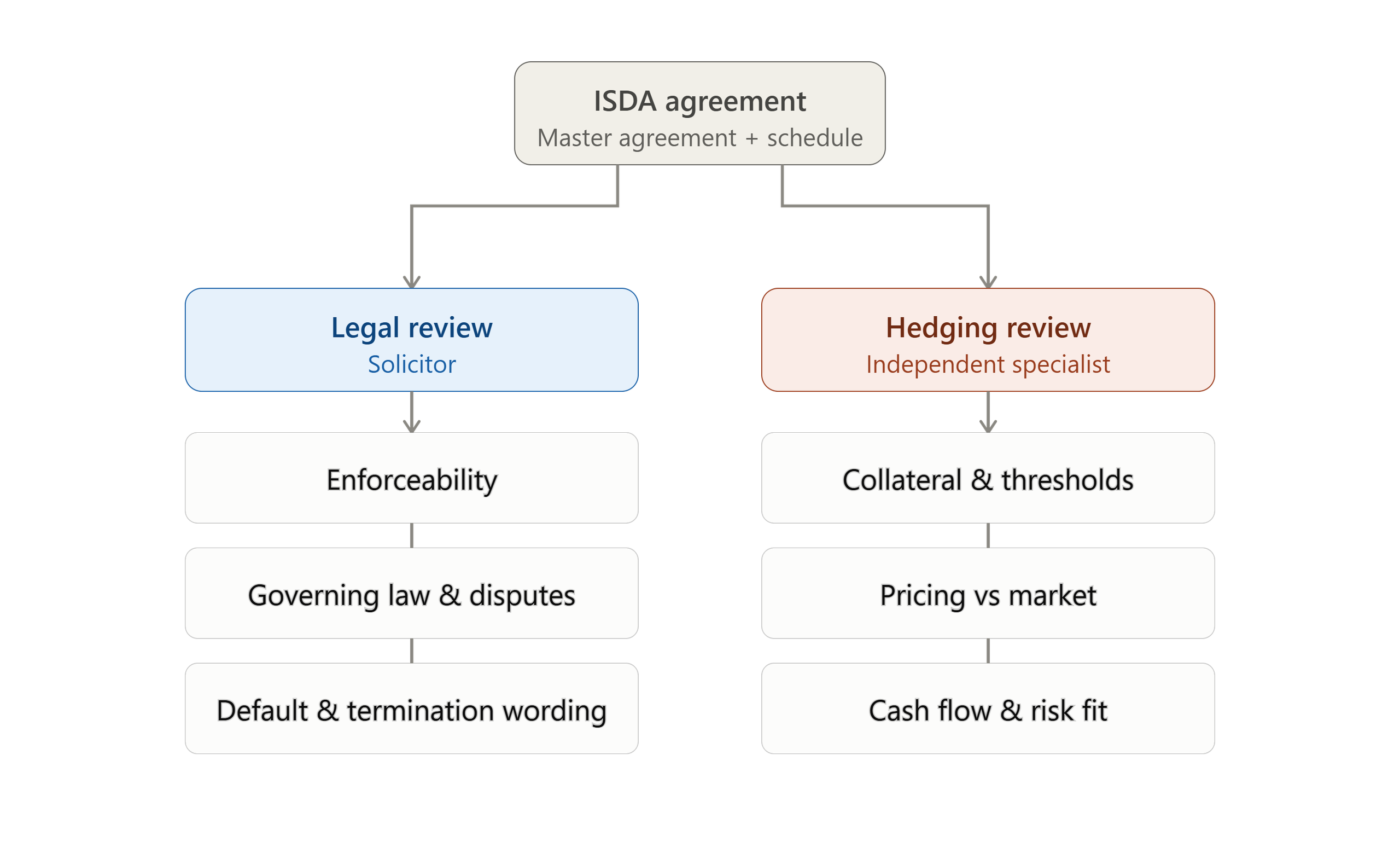

An ISDA is the master agreement that governs derivative trades, like interest rate or currency hedges, between your business and a bank. It’s easy to treat it as just a legal formality: get the solicitors to check the wording and sign. But an ISDA also contains financial terms, around collateral, thresholds, and termination triggers, that decide how much your hedge could actually cost you if things move against you or unforeseen circumstances happen for either the borrower or the bank. For example, we have seen complications when a bank decides to sell down part of the loan to another bank — this causes difficulties for the hedge.

That’s where hedging advice comes in. Solicitors check whether the contract is legally sound. A hedging advisor checks whether the terms themselves are good for your business: how much collateral you might need to post, whether break clauses could catch you out, and whether the deal fits your cash flow and risk appetite. Banks often present their standard ISDA as fixed (pun intended 😂) when in reality many terms are negotiable, but only if you know what to ask for. It is also critical to consider the hedge as part of the business plan, the borrower structure, the facility agreement and, of course, the hedging strategy.

Skip this step, and businesses can end up posting more collateral than expected, facing surprise termination costs, or holding hedges that don’t really match their risk. These aren’t legal failures, they’re financial ones, and they’re avoidable with the right advice before you sign, not after.

Before you sign an ISDA, it’s worth a conversation with Vedanta Hedging to make sure the deal works for you, not just the bank.