Call us on 020 7183 2277

Download LATEST Market Rates >

An Inverted Yield Curve – Why is it so important?

Last week, a part of the US Treasury yield curve inverted for the first time in over a decade. What does this mean and is a recession on the way?

What are US Treasuries?

US Treasuries are debt issued by the US government which pays a fixed rate of interest over a fixed period of time. An investment in a US Treasury bond is generally considered to be one of the safest in the world; the US economy would have to essentially collapse for investors to stop receiving their interest on the treasury bonds.

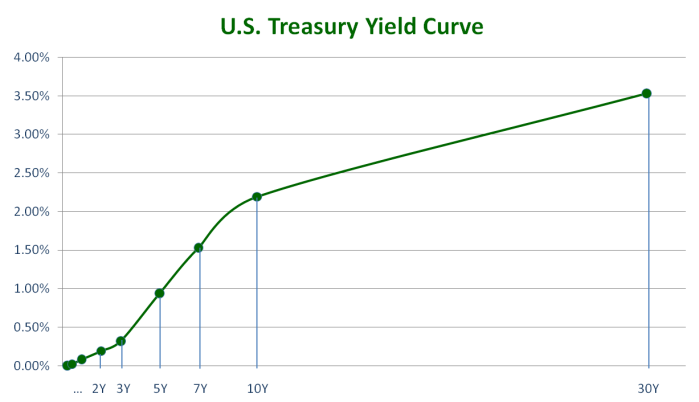

What is a yield curve?

The US Treasury yield curve is a line that plots the interest rates of bonds of similar credit quality but with differing maturities. It is used as an indicator of the economic outlook of the economy. The most common shape of a yield curve is upward sloping: investors of longer-term bonds are compensated for inflation expectations and the risk premium of a longer-term investment. In an upward sloping yield curve, bond investors are signalling to the market that they expect economic growth to continue.

Inverted US yield curve

An inverted yield curve occurs when long-term debt has a lower yield than short-term debt. Short-term investors are requiring a higher return because they are concerned about the outlook in the near-term. An inverted yield curve is often seen as an indicator of an economic recession. In the USA, the 5-year treasury note yield has fallen below the yield on a 3-year treasury note. In other words, the US government is less likely to pay their shorter-term debt than longer-term debt. Though this is not quite as alarming as the inversion of the 2-year and 10-year yields which has preceded the recessions of 1981,1991, 2000 and 2008, there is still cause for concern. This first yield curve inversion in more than a decade raises the question of whether the anticipated rate rise by the Fed will go ahead later this month.

It would be premature to immediately associate the yield inversion with a recession. Recent US economic data including unemployment figures, industrial production and consumer confidence have shown support for a strong real economy. However a rate hike by the Fed this month could be considered to be unwarranted. The 2-year and 10-year yield difference has flattened to 11 basis points. One would assume a potential/upcoming inversion of these yields and a rate rise by the Fed are mutually exclusive. A timing difference between the two may lead to eventual rate cuts in 2019.

What does this mean for the UK?

Stock markets globally have not taken well to this news, and started falling last week as a result of this inversion of the yield curve.

Any potential impact of the above on the UK is currently masked by the House of Commons debate on Theresa May’s Brexit deal (whenever this happens) and the higher-than-comfortable possibility of a no-deal Brexit.

If the Fed were to cut rates in 2019, with the prevailing uncertainty in the UK, it would not be surprising to see the the BOE’s MPC follow suit. This is because the UK interest rate cycle typically follows that of the US.